The global channel SSD market saw a significant slowdown in 2024, driven by weak consumer demand and saturation in the notebook segment. After hitting record-low prices in 2023, SSD pricing began to recover this year, but retail sales continued to struggle. With notebook SSD attach rates already at 100% and consumer electronics demand remaining soft, overall SSD module shipments declined sharply.

Channel SSD shipments for 2024 are estimated at around 101 million units, marking a 14% decline compared to last year.

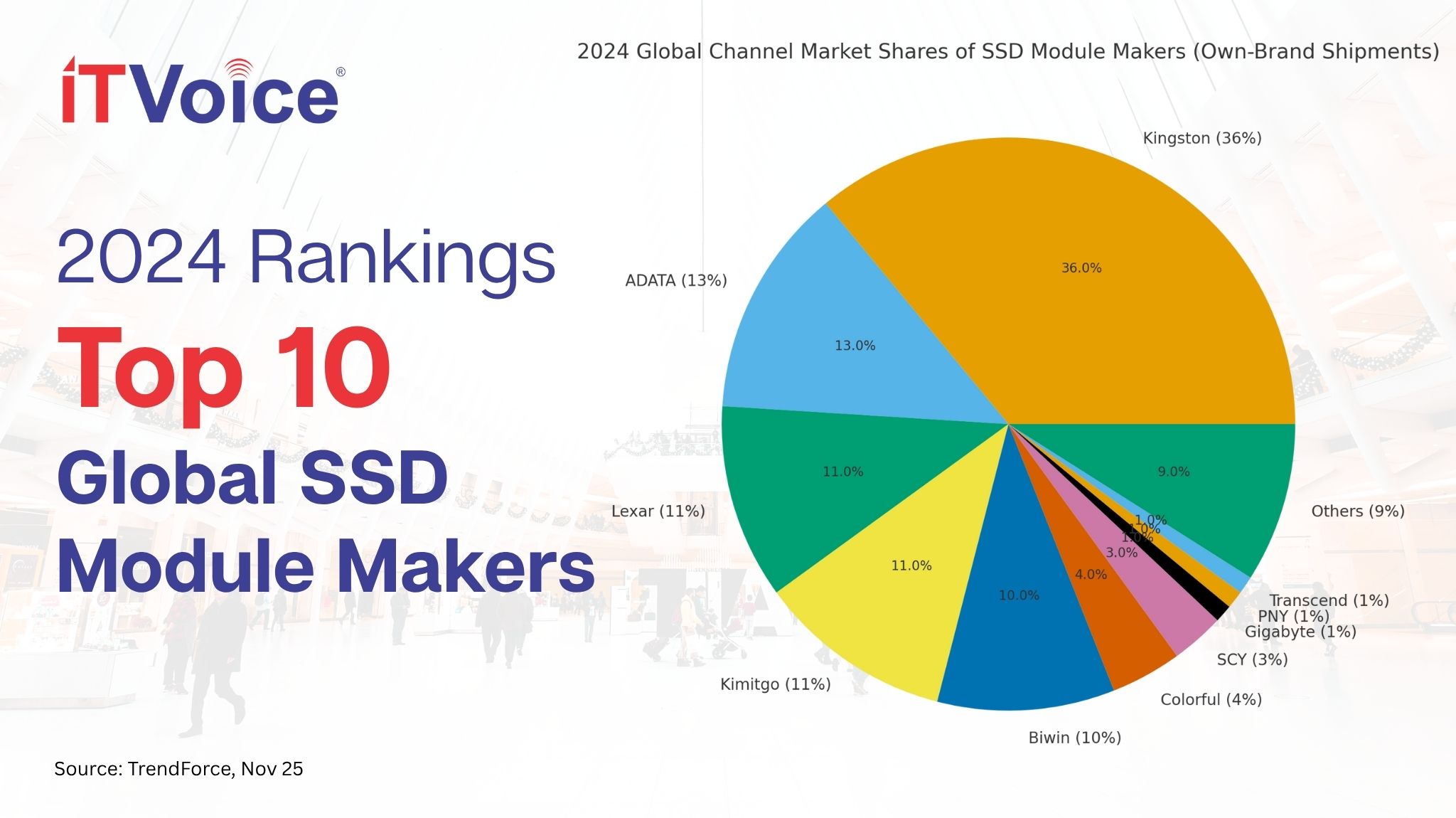

Market Concentration Intensifies: Top Five Brands Dominate

The 2024 rankings for SSD module makers show that the market has become more consolidated than ever, with the top five brands now accounting for over 80% of global channel shipments.

Kingston retained a strong lead with a 36% share, supported by broad channel distribution and a reputation for dependable products. ADATA followed with 13%, boosted by active promotion of gaming and high-performance consumer SSDs and rapid rollout of newer PCIe generations.

Lexar placed third with 11%, continuing to grow across China and international retail markets. Kimtigo and Biwin secured the fourth and fifth spots, each benefiting from strong domestic demand and expanding their presence overseas.

Performance Across Mid- and Lower-Tier Brands

Colorful ranked sixth by maintaining a competitive price-to-performance positioning through in-house NAND and controller development. SCY made its first appearance in the global top 10 at seventh place, reflecting its rising visibility in China’s retail channels.

The remaining positions were held by Gigabyte, PNY, and Transcend. Gigabyte leveraged its gaming ecosystem to retain market traction, PNY performed steadily across North America and Europe, while Transcend continued focusing on industrial and professional-grade storage applications.

AI-Driven Demand Expected to Lift SSD Market in 2025

Industry expectations suggest that 2025 will see renewed growth, led by the rise of AI-enabled PCs, edge AI devices, and demand for higher-capacity, faster SSDs. Brands that enhance their technical capabilities, strengthen channel strategies, and refine market positioning are likely to be better positioned to capture the next wave of demand.

Source: Market data referenced from TrendForce’s 2024 SSD Module Maker Channel Shipment Analysis.